Rep. Campbell's Terrible, Horrible, No Good, Very Bad Bill

Rep. John Capbell, a California Republican, has introduced what may well be the worst Republican-led bill of the current session. His proposal, H.R. 3125 (there's no short title) is a pre-funded bailout for California's state-run, currently privately funded California Earthquake Authority (CEA). It's difficult to overstate how bad an idea this bill is and how much damage it could do to the country. Indeed, it would put taxpayers around the country on the hook for billions of dollars in losses to private homes that they don't currently have to pay.

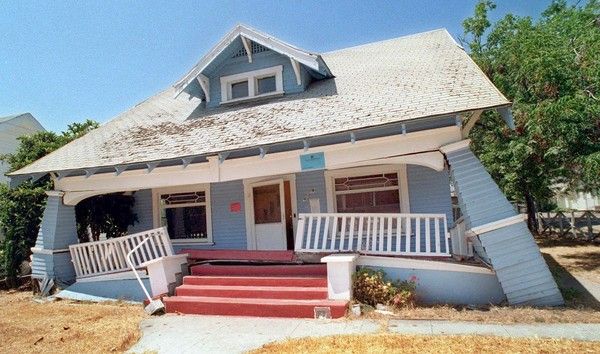

Some background first: CEA, created after a series of earthquakes combined with governmental price controls on quake insurance sent private insurers fleeing from the California earthquake market, exists to write quake insurance for anyone in California who wants it. It's the largest earthquake insurer in the country and, largely because it transfers most of its risk to private reinsurers, is the only large government-run property insurer in the country (about half of states have them) that could pay all of its bills even after a major catastrophe.

The organization is run by experienced insurance industry insiders, provides good services and charges surprisingly low rates: a two story wood framed home in Beverley Hills (90210) with an insured value of $500,000--land costs mean that the house would easily be sell for over $1 million--is insurable for $71.66 a month. Deductibles are much higher than those in the private sector, but low or no-interest Small Business Administration disaster loans could cover all or almost all of them for most individuals.

Take up rates for quake insurance, however, remain very low--about 12 percent--largely because lenders and the government-owned mortgage securitizers (Fannie Mae and Freddie Mac) don't require people to purchase it and many assume, wrongly, that the government would pay for losses after a quake. (The latter wouldn't happen: Except after Hurricane Katrina, government assistance has never paid significant amounts towards rebuilding private homes.)

The bill Campbell has proposed would replace this structure--flawed though it is--with one that gives a federal guarantee to CEA loans in place of the private reinsurance. This scheme, while promised to break even, cannot possible work as advertised because it blatantly crashes the established rules for writing insurance.

Here's why: Insurance works by managing risk across broad pools of events unlikely to happen at the same time. Through private, international reinsurance markets, CEA right now polls the risk of quakes in California with the risks of quakes in Australia, industrial accidents in Japan, and floods in the United Kingdom. Since these events almost never happen at the same time, the reinsurers can make profits off of one type of coverage even when they pay out huge claims on another.

All other things being equal, this means that they can charge less for coverage and still make profits than would insurers that focused their risk in one place. Having the federal government insure against earthquakes through loan guarantees (and, since CEA is the only entity of its type, it would provide such insurance only in California) will mean that, to break even, it will have to charge more than a diversified private reinsurer would. Thus, the federal government will have to either charge more than the private sector which defeats the purpose of the guarantee in the first place or under-price its coverage on an ongoing basis and leave taxpayers holding the bag.

Experience shows that the later is almost sure to happen. The National Flood Insurance Program, probably the most similar current entity now in the federal government, was also promised to break even when Congress created it but currently has run up debts of over $17 billion that it has no way of paying back. The other major federal property insurance program--crop insurance--is arguably worse: it drains about $6.5 billion in subsidies directly from the Treasury.

Quite simply, Rep. Campbell's proposal is a truly awful idea that deserves to be dead on arrival in Congress.